Why is personal insurance important? Claims stats

You’ve worked to give yourself a good income, and your income is going to play a big role in your lifestyle, and that of your family, for a long time to come.

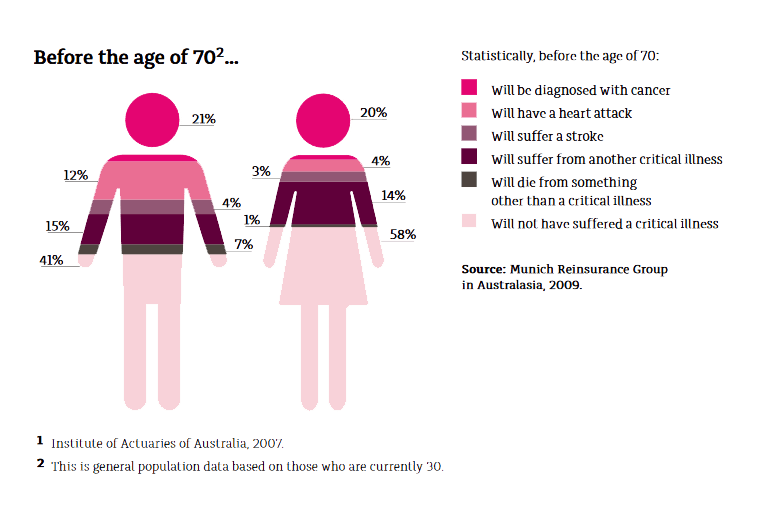

It sounds like something you’d want to protect, right? But under-insurance is an issue facing an alarming number of Australians, from all walks of life.

The insurance we’re talking about is life insurance – the most common forms of which are death cover, total and permanent disability (TPD), trauma insurance and income protection.

Life insurance isn’t just about protecting your family financially if you die. It’s about protecting your lifestyle if you get sick or injured. So if you can’t work for a while, or ever again, you’ve got a financial back-up plan.

Think of all the cases of physical and financial hardship you’ve seen in your profession. Then imagine it was your family that had to go through it all without financial support.

Many people are self-employed, adding another layer of financial responsibility to the equation.

But despite their significant insurance needs, many small business owners are also failing to protect themselves and their families with adequate insurance.

According to a 2006 survey by the Investment and Financial Services Coucil (FSC), less than half of small business owners feel they have adequate cover .

So if they know they’re not properly covered, why aren’t they doing something about it?

One of the reasons is that there's a perception insurance is too expensive.

But think about the sort of money you’d lose if you couldn’t work for a few months. Or worse, if you could never work again. It certainly helps put the cost of insurance into perspective.