Australia is among the worlds most under insured countries in the world. It’s no secret that not enough for Australians to hold life insurance, and recent research in this area has highlighted the issue. Research conducted by TAL, a major industry insurer, has shown that only 30%-70% of Australians aged 18-69 hold life insurance, while only 11%-18% hold disability cover, income protection insurance or trauma (often referred to as critical illness) cover.

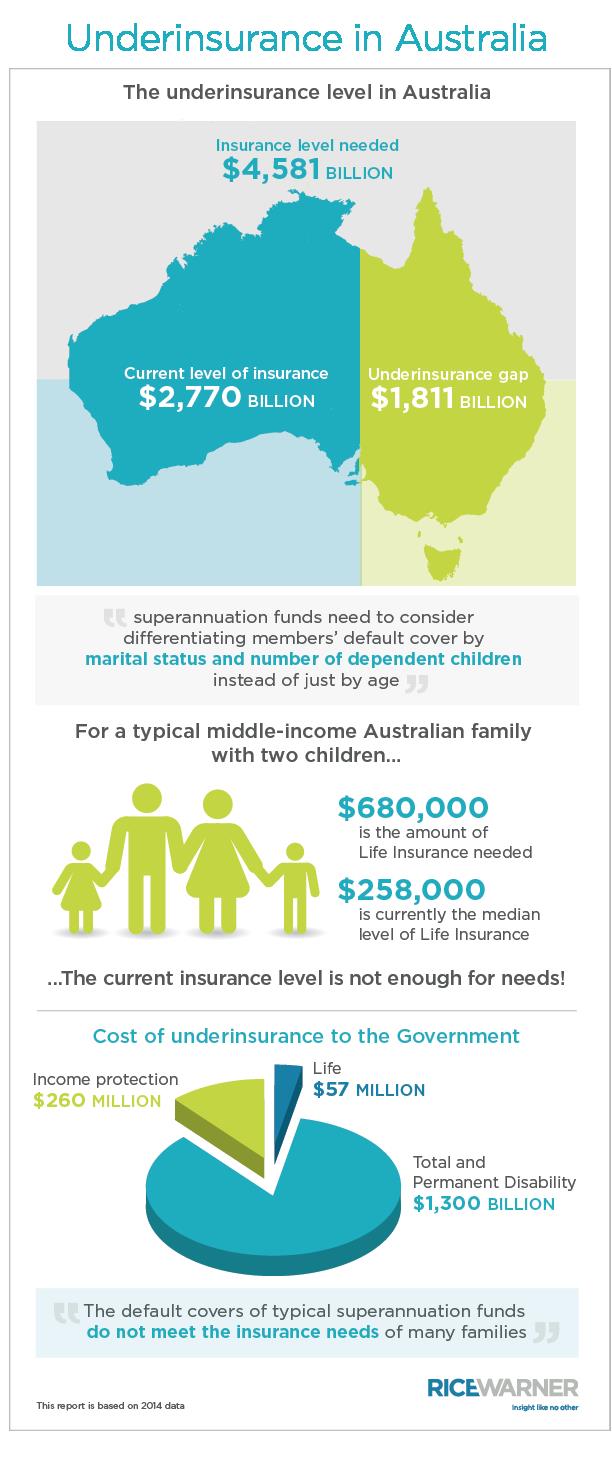

Recent research by Rice Warner found that even amongst those few Australians who currently hold life insurance, we are still grossly under insured – to the extent of $1,811 billion.

The findings showed this was made up of the following:

- $57 million per year for life insurance

- $1,258 million per year for Total and Permeant Disability (TPD) cover

- $260 million per year for Income Protection

“superannuation funds need to consider differentiating members’ default cover by martial status and number of dependant children instead of just by age” – Risk Warner, 2015

The past decade has seen many changes to insurances both in the retail and default cover superannuation base. The default life insurance (relative to average income) contained within superannuation environment has doubled, from 15% to 30%. Whilst we may say this is a great outcome for the under insured problem we play host to in Australia, we still have far to come in regards to overcoming this issue.

The median level of life insurance cover required for young families (i.e. couples in their mid-thirties with young children) is roughly $680,000. However, our nation’s average default cover level only amounts to $200,000, therefore leaving us with a shortfall of approximately $480,000. This is a scenario which plays out for most young families as they are not familiar with and disregard the importance of holding appropriate levels of personal insurance cover.

Planning ahead before starting a family

For those of us without a family, the news is slightly healthier with around 60% of our insurance requirements being covered. Recent studies of the dominant gender for purchasing life insurance found around 60% of women do not have life insurance at present, with many not planning to purchase any life insurance cover before beginning a family. This is alarming as the costs of beginning a family are costly as well as an important time in your life for the family as a collective unit. More reason to think about acquiring life insurance cover! What’s more, to add to this, women were half as likely as men to search for insurance with 70% of life insurance enquiries in 2013 being made by men (*according to RiskInfo Research).

{kind=link}

The birth of a child is the number one prompt to families to think about and discuss life insurance. This is largely due to the events which occur around this time in their life which will usually coincide with events such as the purchase of a family home. Unfortunately, it doesn’t make sense for women to avoid getting life insurance. However, when we look at the data we start to see alarm bells ringing. For example, a 45-year-old woman is 94% more likely to make a disability insurance claim due to sickness than a man of the same age (statistics from the Financial Services Council and KPMG). This should give rise for you to begin the process of looking at life insurance options or speaking with your financial adviser regarding your situation and how best protect you and your family.

The importance and onus lie with you as the individual to ensure you have adequate life insurance cover in place which matches both you and your family’s protection needs for cover. Often your superannuation fund will have a default level of cover inbuilt. Before proceeding with purchasing life insurance you should determine whether or not this level of cover is sufficient for your financial wealth protection. If this is not the case, then you should consider talking with your financial planner to determine the correct level of cover to meet your needs and objectives.

Taking out life insurance cover will ensure you avoid financial hardship and are not required to sell down your capital in the event of your passing. Total Advice Partners can assist with developing your life insurance needs or reviewing your current insurance cover policies. Contact us at any time on (07) 3284 7875 to discuss your options with one of our financial planners.